Many manufacturers assume cyber insurance will protect them after a ransomware attack or cybersecurity incident until they discover they no longer qualify for coverage, fail renewal requirements, or face denied claims due to missing security controls. For manufacturers with 20–100 employees, failing cyber insurance requirements can create serious operational and financial exposure, including increased premiums, rejected claims, prolonged downtime, compliance issues, and recovery costs reaching tens or hundreds of thousands of dollars.

Cyber insurance requirements have changed significantly in recent years, especially for manufacturing companies. Insurance providers now evaluate cybersecurity maturity, backup validation, ransomware protections, operational continuity planning, and infrastructure security before approving or renewing coverage. Manufacturers relying on outdated infrastructure, reactive IT support, or incomplete cybersecurity controls are increasingly exposed to coverage gaps and operational risk.

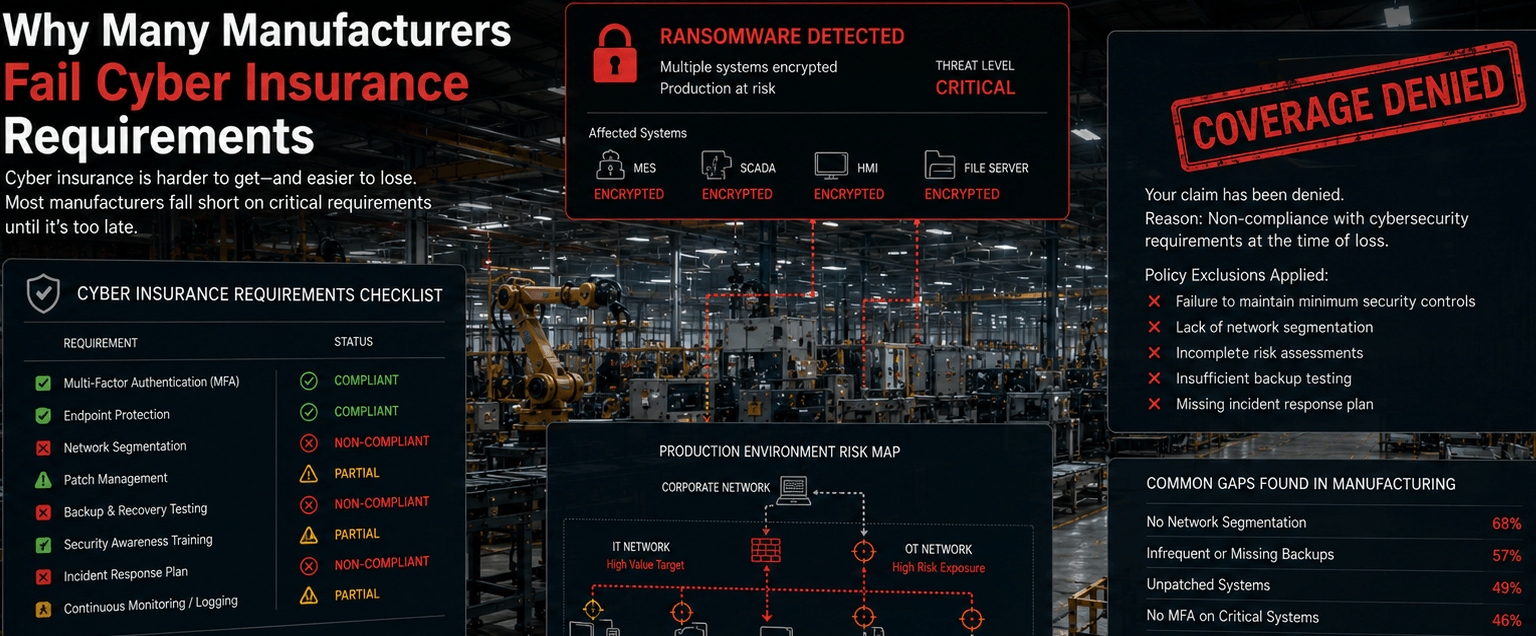

The 7 Most Common Reasons Manufacturers Fail Cyber Insurance Requirements

Many manufacturers believe basic antivirus software and backups are enough to satisfy insurers. In reality, modern cyber insurance requirements now focus heavily on operational resilience and ransomware readiness.

1.Multi-Factor Authentication (MFA) Is Missing or Incomplete

MFA is now one of the most commonly required cybersecurity controls. Insurance providers increasingly require MFA for:

- email systems

- remote access

- VPN connections

- administrative accounts

- cloud platforms

- ERP environments

Manufacturers frequently fail requirements because:

- MFA is optional instead of enforced

- legacy systems lack MFA support

- remote vendors bypass protections

- shared accounts remain active

Missing MFA is one of the fastest ways to trigger denied coverage or higher premiums.

2.Backups Exist But Recovery Testing Is Never Performed

Insurers increasingly evaluate:

- backup reliability

- restore validation

- ransomware recovery readiness

- disaster recovery planning

Many manufacturers run backups daily, receive success alerts, and assume recovery will work without testing ERP restoration, production file recovery, and operational recovery timelines.

Backups that cannot support operational recovery may not satisfy cyber insurance expectations.

3.Aging Firewalls and Unsupported Infrastructure Increase Risk

Many manufacturing environments still operate:

- unsupported firewalls

- outdated VPN appliances

- unpatched servers

- aging switches

- legacy operating systems

Insurers view unsupported infrastructure as elevated ransomware exposure, increased operational risk, and reduced recoverability.

Aging infrastructure significantly increases cybersecurity underwriting concerns.

4.Flat Networks Allow Ransomware to Spread Easily

Many manufacturers continue operating unsegmented networks where office systems, production systems, backups, warehouse systems, and engineering workstations all communicate freely.

Insurance providers increasingly evaluate:

- network segmentation

- ransomware containment

- operational isolation protections

Flat networks create major operational and cybersecurity liability.

5.Endpoint Security and Monitoring Are Insufficient

Manufacturers often rely on traditional antivirus only, outdated security tools, reactive monitoring, and limited visibility.

Modern insurers increasingly expect:

- Endpoint Detection & Response (EDR)

- centralized monitoring

- ransomware detection

- continuous threat visibility

Limited monitoring capabilities increase both breach risk and recovery costs.

6.Incident Response and Disaster Recovery Plans Are Missing

Many manufacturers lack documented procedures for:

- ransomware response

- operational recovery

- communication escalation

- backup restoration

- vendor coordination

Insurers increasingly evaluate incident response readiness, recovery documentation, and operational continuity planning.

Operational preparedness now matters as much as cybersecurity prevention.

7.Employees Remain Vulnerable to Phishing Attacks

Phishing remains one of the most common ransomware entry points. Manufacturers frequently lack:

- phishing awareness training

- email filtering protections

- user security policies

- simulated testing programs

Human error remains one of the largest cybersecurity risks insurers evaluate.

Why Cyber Insurance Requirements Became Stricter for Manufacturers

Manufacturing has become one of the most targeted industries for ransomware and operational disruption.

Why Insurers View Manufacturers as High-Risk

1.Operational Downtime Creates Financial Pressure

Manufacturers rely heavily on:

- continuous production

- shipping schedules

- inventory synchronization

- ERP coordination

Attackers know downtime pressure creates urgency.

2.Legacy Infrastructure Creates Cybersecurity Gaps

Many manufacturing environments still contain:

- unsupported systems

- insecure remote access

- outdated network devices

- weak segmentation

3.Recovery Costs Continue Rising

Cyber incidents increasingly create:

- prolonged downtime

- operational backlog

- recovery consulting costs

- legal and compliance expenses

- reputational damage

4.Ransomware Continues Evolving

Modern ransomware attacks increasingly target:

- backups

- production systems

- operational infrastructure

- remote access environments

Cyber insurance providers now evaluate operational resilience, not just technical controls.

What Cyber Insurance Providers Usually Evaluate?

Most insurers now require manufacturers to demonstrate multiple layers of cybersecurity and recovery readiness.

Common Manufacturing Cyber Insurance Requirements Checklist

Access Security

- MFA enforcement

- Unique user accounts

- Administrative access controls

- Password policies

Infrastructure Security

- Supported firewalls

- Patch management

- Endpoint protection

- Network monitoring

Backup & Recovery

- Offsite or immutable backups

- Restore testing

- Disaster recovery procedures

- Recovery timeline documentation

Operational Resilience

- Network segmentation

- Incident response plans

- Vendor risk management

- Operational continuity planning

User Protection

- Phishing awareness training

- Email filtering

- Security awareness policies

Manufacturers lacking even a few of these controls may face increased premiums or denied coverage.

The Operational Consequences of Failing Cyber Insurance Requirements

Textile Manufacturer

A textile mill failed cyber insurance renewal due to:

- missing MFA

- outdated VPN infrastructure

- incomplete backup testing

Operational impact:

- increased premiums

- delayed renewal approval

- pressure to modernize infrastructure quickly

Beverage Manufacturer

A ransomware incident exposed backup recovery gaps during an insurance investigation.

Operational impact:

- extended production downtime

- delayed claim processing

- uncovered recovery expenses

Root cause:

- restore procedures had never been validated

Plastics Manufacturer

An insurer identified unsupported firewall infrastructure during underwriting review.

Operational impact:

- higher renewal costs

- required remediation deadlines

- operational cybersecurity review

Many manufacturers discover cybersecurity weaknesses only during insurance audits or incidents.

How Manufacturers Improve Cyber Insurance Readiness

Manufacturers that maintain strong insurability typically focus on operational resilience and layered cybersecurity maturity.

The 5-Layer Manufacturing Cyber Insurance Readiness Framework

1.Enforce MFA Across Critical Systems

Manufacturers should require MFA for:

- remote access

- cloud platforms

- ERP systems

- administrator accounts

2.Modernize Aging Infrastructure

Manufacturers should evaluate:

- unsupported firewalls

- outdated VPNs

- aging servers

- insecure remote access systems

Unsupported infrastructure creates major underwriting concerns.

3.Validate Backup and Recovery Readiness

Manufacturers should regularly test:

- backup restores

- ERP recovery

- operational recovery timelines

- disaster recovery workflows

4.Improve Network Segmentation and Monitoring

Manufacturers should:

- isolate production environments

- separate backups

- monitor operational traffic

- deploy endpoint detection tools

5.Build Operational Incident Response Procedures

Manufacturers should document:

- ransomware response plans

- operational recovery priorities

- communication escalation procedures

- vendor coordination workflows

Insurers increasingly evaluate operational preparedness, not just technical protections.

Warning Signs Manufacturers Should Not Ignore

Manufacturers should immediately review:

- Unsupported firewall or VPN infrastructure

- Missing MFA enforcement

- Untested backups

- Shared user accounts

- Flat production networks

- Limited endpoint monitoring

- Outdated incident response procedures

- Increasing phishing incidents

Cyber insurance issues often reveal larger operational cybersecurity weaknesses.

Illustrative Scenario: Manufacturer Fails Cyber Insurance Renewal

A 50-employee beverage manufacturer in Los Angeles underwent cyber insurance renewal after experiencing increased insurer scrutiny.

During the assessment, the insurer identified:

- incomplete MFA enforcement

- unsupported firewall infrastructure

- limited backup testing

- flat production network architecture

Although the company had antivirus software and backups in place, insurers determined the environment lacked sufficient ransomware resilience.

The manufacturer faced significantly higher premiums, delayed renewal approval, and mandatory remediation requirements. After implementing MFA enforcement, firewall modernization, segmented backups, endpoint monitoring, and recovery validation testing, the company improved its cyber insurance posture and reduced operational cybersecurity risk.

Why Work With an IT Provider That Understands Manufacturing Cyber Insurance Requirements?

Manufacturers should work with IT providers that understand:

- ransomware exposure in manufacturing

- operational downtime risk

- cyber insurance underwriting expectations

- production continuity planning

- recovery readiness

- manufacturing cybersecurity architecture

Cyber insurance readiness now depends heavily on operational resilience, not just IT checklists.

Trust Signals

Fothion supports manufacturing companies that require:

- cybersecurity-first operational environments

- ransomware resilience strategies

- proactive infrastructure modernization

- backup and disaster recovery planning

- operational continuity protections

- manufacturing-focused IT strategy

With over 20 years of experience (since 2001), Fothion helps manufacturers strengthen cybersecurity readiness, improve insurability, and reduce operational downtime risk.

Get a Manufacturing Cyber Insurance Readiness Assessment (30 Minutes)

If you’re unsure whether your manufacturing environment would satisfy modern cyber insurance requirements, the fastest next step is identifying your biggest cybersecurity and recovery gaps.

Book a 30-minute call with Fothion and we’ll:

- review insurance-related cybersecurity risks

- assess ransomware exposure

- evaluate backup and recovery readiness

- identify operational vulnerabilities

- outline practical ways to improve insurability and resilience

Book here: https://fothion.com/schedule-a-phone-call/

FAQs (with answers):

1.Why are manufacturers failing cyber insurance renewals?

Many manufacturers fail renewals due to missing MFA, untested backups, unsupported infrastructure, weak segmentation, and insufficient ransomware protections.

2.What cybersecurity controls do insurers require most often?

Common requirements include MFA, endpoint protection, backup testing, network monitoring, incident response planning, and supported firewall infrastructure.

3.Can cyber insurance claims be denied after ransomware attacks?

Yes. Claims may be denied or reduced if required cybersecurity controls were missing or operational recovery readiness was insufficient.

4.Why do insurers consider manufacturers high-risk?

Manufacturers are heavily targeted by ransomware because operational downtime creates urgency and recovery costs can become extremely expensive.

5.How can manufacturers improve cyber insurance readiness?

Manufacturers can improve readiness through MFA enforcement, infrastructure modernization, backup testing, segmentation, endpoint monitoring, and disaster recovery planning.

6.Are backups enough to satisfy cyber insurance requirements?

No. Insurers increasingly expect restore validation, ransomware resilience, operational recovery planning, and documented recovery procedures, not just backup existence.